Standardizing Appraisals for PV Installations

Geoffrey T. Klise

1

, Jamie L. Johnson

2

, and Sandra K. Adomatis

3

1

Sandia National Laboratories, Albuquerque, NM, 87185, USA

2

Energy Sense Finance, LLC, Punta Gorda, FL, 33980, USA

3

Adomatis Appraisal Services, Punta Gorda, FL, 33951, USA

ABSTRACT — As PV installations increase across the U.S.,

there will be a point when an appraiser will have the opportunity

to value the PV system as part of a property sale or re-finance.

Proper valuation techniques as applied to solar PV are necessary

to reflect the increase in market demand for solar PV systems.

Appraisers must follow the Uniform Standards of Professional

Appraisal Practices (USPAP) when valuing solar PV systems,

which means that appraisers must gain competency to 1)

accurately recognize the value proposition of a PV system, and 2)

develop the PV system’s market value as it contributes to the

property. The challenges currently faced by property owners

with installed PV are whether the PV system adds market value

to the property, and finding an appraiser with competency. Not

all markets are the same, and PV market values will vary

considerably based on many factors that include, but are not

limited to the adoption rate in the particular market, the utility

rate paid by the customer, the PV system’s condition, aesthetics,

and obsolescence. This paper will discuss how past challenges

with respect to proper PV system valuation are being addressed

in a standard fashion, along with the far-reaching benefits that

may be available to future PV adopters as valuation concepts are

ultimately recognized and adopted by valuation professionals,

real estate agents, mortgage lenders and underwriters.

Index Terms — photovoltaic systems, appraisal, market value,

fair market value, property transaction

I. INTRODUCTION

There is currently a great deal of effort being made to

increase the adoption rate of solar photovoltaic (PV) systems

across the U.S. by focusing research to provide solutions that

reduce both the hardware (balance-of-system) and soft

balance-of-system, or “soft costs” of an installed PV system.

In the area of reducing soft costs related to financing as

defined by the SunShot Vision Study [1], a strategy to achieve

cost goals includes “Expand access to a range of business

models and financing approaches.” Directly related to the

effort at reducing financing costs is the ability to access lower

cost financing, which indicates that lower cost financing is

available, however barriers must be overcome to open up

these products to those interested in financing a PV system.

The current higher capital cost for financing and inability to

access lower rates reflects the potential risk premium

perceived by some lenders of both unsecured and secured loan

products used to purchase PV systems, as well as their relative

lien position.

One area that has not received as much attention in terms of

the potential to reduce soft costs has to do with how a PV

system is valued in a residential or commercial property

transaction. Because PV systems are arguably still in the early

adopter’s phase of Roger’s Bell Curve and are not common

across the US [2], most appraisers are unsure about the market

value proposition it can provide to property owners. It is this

lack of understanding (due to market immaturity and lack of

education opportunities), and lack of both support and

understanding from lenders, underwriters and government

sponsored enterprises (GSE’s) that has led to improper

valuation techniques as applied to PV systems. It also holds

true that not every market has been educated on the benefits of

PV systems, which is borne out in how local markets respond

either positively or negatively to estimates of value.

Reconciling these challenges to support the proper valuation

of PV systems through education efforts aimed at the real

estate and valuation professionals will ultimately result in the

recognition of the fact that an increase in market acceptance of

PV systems is occurring throughout the U.S. The value

proposition enjoyed by current PV owners will over time be

better understood by future PV adopters and those in the

appraisal, real estate and lending industries. This recognition

will translate into lower perceived risk and greater access to

lower cost financing.

This paper will discuss the efforts to have PV systems

recognized in real property appraisals being led by a number

of groups that include private industry, professional

organizations and national laboratories. Examples of standard

appraisal practices will be presented, along with areas of

existing research and education efforts currently underway

that are designed to gain access to lower financing and reduce

existing financing costs through the support of the real estate

and valuation industries.

II. IMPORTANCE OF PROPER PV SYSTEM VALUATION

One of the main benefits to a homeowner that owns a PV

system is the fact that once a PV system is given value in a

property sale or re-finance, that value is essentially ‘unlocked’

allowing the owner to realize some of the initial investment in

the PV system, especially if the payback of the PV system has

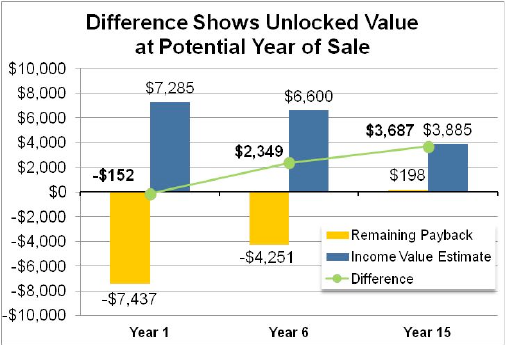

not been realized. Fig. 1. The fact that some PV systems have

not been properly appraised or the market did not support the

value through comparable sales, results in situations where for

example, the property was sold with the PV system, but the

payback from the investment was never realized and an

economic loss to the original PV system purchaser may have

occurred. Figure 1 indicates that in year 6, if the value is

recognized, yet payback has not yet occurred, using an income

based discounted cash flow approach, that remaining payback

has been recovered. Standard appraisal practices in support of

transactions with knowledgeable buyers and sellers can

facilitate the unlocking of the PV system’s value and remove a

barrier that many potential adopters experience have when

selling their home before the payback is reached.

Fig. 1 Example of value unlocked from a 2.4 kW PV system with

a net cost of $7,631 and a payback (as a function of utility bill

savings) around year 14. PV system value determined using PV

Value® tool, payback (simple) calculated using SAM.

It is also important for appraisers to understand ownership

of the PV system, as that will determine if value can be

developed and what other components of value may have to

be considered.

PV systems in states with fixed contract renewable energy

credits or certificates (REC), and production based incentives

can add value based on the guaranteed income stream. Other

states that have these RECs that can be sold or traded in REC

markets have varying prices, making it difficult for an

appraiser to consider value beyond what the REC is worth at

the time the appraisal is completed. A proper understanding of

these differences will ensure value is developed correctly.

III. HOW PV SYSTEMS ARE APPRAISED

This section will discuss concepts around appraising PV

systems, provide examples of early practices, and show

standard practices are currently being implemented.

Appraisers use variations of three approaches: cost, income

and sales comparison [3] to develop the potential market

value. Most importantly, they must demonstrate “competency”

before accepting an assignment otherwise they must acquire

competency during the assignment or “withdraw from the

assignment” [4]. However, if the appraiser’s client is selling

the loan on the secondary mortgage market that falls under the

Government Sponsored Enterprises (GSEs) such as Fannie

Mae or Freddie Mac, the appraiser must have competency

prior to accepting the assignment [5]. These guidelines

indicate the appraiser must have knowledge of the PV

systems, understand how PV systems work and have sufficient

appraisal methodology knowledge to complete the

assignment.

In the early 1980s, appraisers published papers that

suggested using combinations of a cost and income approach

to estimate the value of a PV system, recognizing back then

there were not enough comparable properties with solar to use

a paired sales approach [6] [7]. Those observations still hold

true today; comparable properties with PV are still far and few

between making it difficult for an appraiser to weigh the

market for PV systems on comparable properties alone.

A. Comparable Sales

A typical comparable sales analysis traditionally utilized by

an appraiser compares the subject property to other similar

properties nearby, and within a specific timeframe. As solar is

a new feature, an appraiser relying on comparable sales may

not find a PV system and erroneously conclude that since no

existing homes sold with PV nearby within a certain time-

frame, there is no market demand or support for value. Some

underwriters are insisting on no value placed on a PV system

if the appraiser cannot find a sale of a similar property that has

a PV system. As appraisers are required to also consider cost

and income approaches [3], a comparable sales only approach

may not be appropriate in most U.S. markets.

A comparable sales analysis that reveals homes sold with

solar PV could be conducted. Understanding the

characteristics of the PV system is necessary to make

adjustments to comparable sales based on the differing size of

the PV system. It is highly unlikely that each comparable will

have the same size PV system; and therefore, the value of the

produced energy would have to be determined to make a

proper adjustment. This is also important considering whether

the PV system is working optimally, or if it is being shaded

and output is reduced. Evaluating the condition of the

comparable PV systems would alleviate these concerns,

however, data may be difficult to obtain.

A large study in California completed by Lawrence

Berkeley National Laboratory compared sales of homes with

PV and without to determine what premium, if any, existed on

homes sold with PV systems. Their results indicated that

depending on whether the home was new construction, or

existing, the price per watt premium varied between $2.30 -

$2.60/watt, and $3.90 and $6.40/watt, respectively for homes

with PV systems, as compared to comparable homes without

PV [8]. Energy savings was not analyzed in this study, though

estimates in California were used to develop a ratio. It is worth

mentioning that the premium identified in this study could

also include other features or condition of the homes, which

were not completely disentangled from the value of the PV

system. In addition, there was no information that stated what

method appraisers used to develop value. As this study

presented premiums in California for a limited sample size,

this data shows evidence of market reaction to PV systems,

however, relying exclusively on these premiums is not an

acceptable basis for the value of the PV system without other

appraisal techniques. An appraiser should understand the PV

system’s condition, existing market demand and other factors

necessary to develop the PV system’s contributory value to

the property.

B. Cost

The Cost approach is a way of developing value though an

understanding of what it would cost to replace the item. The

age-life method is one way that residential appraisers can use

a cost approach. The challenge when using this approach for

an appraiser, which currently limits its effectiveness, is the

presence of many different types of rebates and tax credits,

some of which can only be used one time by the property

owner.

This method is shown in Table 3 in the comparison of

different appraisal techniques for a residential property. As the

PV modules have a 25-year useful warranty life, the age of the

system is divided by the useful life (physical age/life method)

to return a depreciation percentage. This amount is then

multiplied by the cost of a system purchased today less

incentives except tax related incentives to apply the

depreciation amount, which is then subtracted from the cost to

get the final depreciated value. However, this method only

addresses the physical depreciation and requires the appraiser

to consider obsolescence that exists in markets where cost

exceeds what the market is willing to pay. This results in a

superadequacy. The physical age/life method does not include

the obsolescence; therefore, the appraiser must measure the

obsolescence and also subtract it from the cost. Due to each

individual’s different tax rate, the use of tax credits in a

depreciated cost framework is not recommended for

developing a market value for the PV system [9].

The appraiser must always consider cost of the PV System

as of the effective date of value and not the cost paid by the

purchaser when it was new. Therefore, with the cost of PV

systems decreasing, the cost may eventually not have the

problem of a superadequacy to consider. Also, if the PV

system is not working “optimally” due to shading or other

issues, this approach may result in a value estimate that is too

high unless the appraiser can adjust the physical depreciation

to account for the physical deficiency.

C. Income Approach - Gross Rent Multiplier

A Gross Rent Multiplier (GRM) is essentially a simplistic

income capitalization approach to translate the value of a

monthly energy savings from energy efficient features into a

contributory value, or adjustment to value [10], based on the

appraisal technique of dividing the sales price of a building by

the monthly rent, which is then multiplied by the monthly

energy savings. The GRM is property specific and is discussed

as an appropriate technique to develop value for energy

efficient features. Having rental data nearby is necessary,

though a proxy method could be developed for that market.

Efforts were made to tie a study about energy efficiency in

the 1990s [11] to the value of PV systems. This metric has

been used by installers and touted as evidence that every

dollar of energy saved by using a PV system translates to an

increase in property value of $20, though this was disputed

[12] based on the premise that applying this ratio to PV

systems (which generate electricity) from a study where PV

systems were not analyzed does not provide enough support to

suggest a 20:1 premium for houses with PV systems. This

type of study is good for finding evidence of value in a certain

market at a certain time period; however, studies do not

necessarily apply to all markets, and would not satisfy USPAP

requirements if relied on solely to develop value.

Can a Gross Rent Multiplier (GRM) be applied to solar PV?

It is possible; however, the appraiser must not rely solely on

this method. This method is one tool from the appraiser’s

toolbox that must be used along with other methods and

reconciled to mirror the reactions of buyers and sellers in the

market.

D. Income Approach – Discounted Cash Flow

Currently, based on the challenges presented with the other

approaches and the unique ‘income’ producing features of a

PV system, an income approach using a discounted cash flow

(DCF) to develop the present value of the energy produced is

a recommended technique.

The benefit of this approach is that it considers the details of

the PV system, and validates whether it is working correctly

and delivering electricity as designed. For a residential

appraiser, this approach can take more time and effort to

perform, however if the data is available, an estimate of value

can be made quickly. The key here is that an appraiser needs

knowledge of how a DCF works, how to set one up properly

and how to provide support for each input. One minor error in

the DCF can result in a larger error in value.

The PV Value® tool (www.pvvalue.com) developed in

2012 as a proof-of-concept that can help appraisers use the

DCF approach as it has the necessary inputs for an appraiser

to develop a value for the PV system [13] [14]. Due to the

challenges with the other approaches, the tool is being widely

used across the U.S., with over 2500 downloads in the past 18

months, and early evidence that appraisers are successfully

utilizing it in appraisals. Current collaboration with LBNL

will involve validating the methodology using existing sales

data in multiple U.S. markets.

With this greater level of accuracy in translating energy

produced to a market value, what are the typical parameters

needed by an appraiser to develop the value? An appraiser

needs the following:

• zip code

• system size

• degradation rate

• derate

• tilt

• azimuth

• discount rate

• utility rate & utility escalation rate

• estimate of O&M expenses, and

• system age.

Many of the parameters in PV Value® including the utility

rate, utility escalation rate and O&M expenses are pre-

determined, however the appraiser can overwrite that data

with more accurate estimates that may be necessary for the

market that is being considered. The discount rate is

determined using a risk-free rate tied to the Fannie Mae daily

Net Yield rates for 15-and 30-year mortgages. These were

chosen for residential appraisals as these rates are most

reflective of the always fluctuating cost to borrow money at

the time the appraisal is conducted. The basis point spread on

top of that risk free rate can be changed by the appraiser if

needed, to reflect other market conditions that speak to issues

around obsolescence, PV system condition, roof repair,

shading, and markets that are supportive, or not supportive of

PV. The resulting Appraisal Range of Value Estimate

provides the appraiser with a general range to use along with

other methods to reconcile to a value contribution for the solar

PV system.

What are the biggest challenges for appraisers when using

this tool? Appraisers and underwriters first need to understand

how a discounted cash flow analysis works. Currently, with

the exception of a few residential appraisers and underwriters

that understand how to value accessory dwelling units and

apartments, most all residential appraisers and underwriters

rely exclusively on the sales comparison approach. USPAP

guidelines do not say that the sales comparison approach is to

be exclusively used for residential properties, therefore the use

of an income approach to develop the contributory market

value to the property is valid. USPAP states all applicable

methods should be used. An appraiser should explain when

reconciling their report, whey he/she did not use an income or

cost approach according to USPAP.

Underwriters often reject the use of the income approach for

the solar PV; however, the appraiser should be the one making

the decision on which approach(s) are applicable and not the

underwriter. The use of this tool (DCF) will help standardize

the appraisal process, especially for residential properties if

the market data reveals it mirrors the reaction of buyers and

sellers. Improvements to the other approaches can be made

over time as the PV industry matures with more PV systems

installed, subsidies and tax credits decrease and education

efforts aimed at the appraisal and real estate industry resulting

in a greater understanding of PV system benefits.

IV. HOW DOES THIS APPLY TO THIRD-PARTY OWNED PV?

Many homeowners believe a PV system adds value to their

property, and as shown above, it does for customer owned

systems. However, does this hold true for third party owned

systems? Much of the answer lies in the difference between

residential and commercial underwriting and the ability to

recover collateral if the PV system is removed from the

property.

For commercial systems, the PV system can be located on

the rooftop, with the building owner charging rent for the use

of the space by the third party PV system owner. This rent can

be capitalized and a value developed by an appraiser. The

Appraisal Institute course materials for valuing PV systems

have many more case studies that discuss how an appraiser

can develop value for PV systems on commercial rooftops,

considering different ownership structures and PPA

agreements [9].

For a residential property with a third-party owned PV

system, the customer is not “renting” their rooftop to the third

party owner to generate income, they are renting the

equipment or entering into a power purchase agreement to

reduce their electricity bill and pay for the use of the PV

system to attain that savings. When a PV system is included in

a valuation estimate, the underwriter will carefully analyze the

additional value developed by the appraiser. In some cases,

the underwriter may exclude the value even if the appraiser

attributes value to the system. For third-party owned PV

systems, the PV system will most likely be listed as an asset

on the Lessors balance sheet and can be removed subject to

the terms of the lease or PPA agreement as it is not owned by

the homeowner.

If an appraiser develops a value based on the energy

produced by the third party owned system, this could also

create a problem in a foreclosure if the PV system were

removed between the time of valuation and time of

foreclosure. Once removed, that collateral evaporates with no

remedy for the lender, and no future energy production for a

potential home purchaser.

A. Fair Market Value

What is fair market value (FMV), and how does it differ

from the market value of a PV system? Related to PV systems,

this is a new opportunity for appraisers that is different from

the way an appraiser considers market value, as a fair market

value appraisal for solar PV may be done to satisfy the tax

rules and regulations when property is transferred between

owners; in the case of PV systems, when a third party owned

PV system is purchased by to the homeowner or is removed

and re-sold by the third party.

FMV can be determined by the appraiser, with an

understanding that this is a transaction between a willing

buyer and seller. When a lease is broken either due to early

buyout clauses, home sale (if home buyer does not want to

assume the PV system lease terms), end of lease term or early

termination, there are opportunities for an appraiser to help

develop that fair market value. The result may be the same or

different from the market value. An appraiser may consider

the cost of a new PV system in their analysis, or the remaining

useful lifetime of the existing system using a tool such as PV

Value®. It is important to note that in many current lease

contracts, the value ultimately paid by the customer in these

transactions is the higher of the value in the buyout or early

termination table within the lease terms, or the fair market

value determined by an independent appraiser.

Ultimately, as more lease transactions enter these potential

ownership transfers and appraisers are brought in to determine

fair market value, a better understanding how this value is

developed can be analyzed and conveyed to help standardize

the process by which appraisers conduct FMV determinations.

V. EXAMPLE RESIDENTIAL APPRAISAL

In this section, an example of an appraisal is presented

along with a treatment of value developed using comparable

sales, cost and income approaches. This is intended to

illustrate how an appraiser should consider the three

approaches when developing value. For the sake of discussion,

there are multiple assumptions here that will vary depending

on the market, as this does not represent an actual appraisal of

a home with a PV system, the available listing data, and the

varying knowledge of buyers and sellers in different markets.

For this example, a house with PV is listed on the market. It

has a 6 kW, 5-year old PV system, no shading and performs as

designed, according to the homeowner. The local MLS system

that this home is entered into just recently adopted fields that

match the Appraisal Institute’s Green Addendum [15] with PV

fields that also match the inputs in the PV Value® tool. The

appraiser that accepts the assignment has taken courses on

valuing PV systems and has appraised property with PV

systems prior to this assignment, and therefore, meets the

definition of having competency according to USPAP and

GSE rules. Details on the price paid for the example PV

system and today’s price are shown in Table 1.

TABLE 1

SUBJECT PROPERTY PV SYSTEM CHARACTERISTICS

Size

Age

Price paid

$/Watt

Gross

cost

Net cost

6 kW

5 yr

$7.00

$42,000

$40,000

a

If purchased 6 months ago

b

6 kW

6 mo.

$4.25

$25,500

$16,450

c

If purchased now – current estimated costs

b

6 kW

0 yr

$4.00

$24,000

$15,400

c

a - Installed before 2009, cap on federal tax credit was $2,000.

b - From appraiser survey of local installers.

c - The utility offers a $2,000 rebate. Current federal tax credit is

$30% with no cap.

A. Information Discovery

The appraiser starts searching for comparable properties to

value just the property without the PV system, and found that

one property that has sold within the past 6 months had a PV

system; however, none of the other houses had a PV system.

The comparable property is listed in Table 2. Since the more

detailed data that is now available in this local MLS

(following AI Form 820.04) was not implemented and

available when the comparable property sold, there were no

information fields that captured the PV system characteristics.

Fortunately, the appraiser knew where to potentially find

information on PV systems, and discovered that a permit was

pulled 3 years ago to install a 4.5 kW PV system on that

comparable property, with a listing of the installing company.

Research revealed there were no rebates offered when it was

installed but there is one currently offered and that the

investment tax credit of 30% was applied with no cap. During

the drive-by of Comp 1, the appraiser also noticed shading on

the PV system during the mid-day, realizing that will reduce

the PV system production.

TABLE 2

COMPARABLE PROPERTIES

1

Subject

Comp 1

Comp 2

Sold Price

N/A

$220,000

$204,000

Date Sold

N/A

6 mo. ago

5 mo. ago

PV System

6 kW

4.5 kW

none

Age of PV

System

5 yrs.

3 yrs.

N/A

Current

Installed Cost

(date of sale)

$4.00/Watt

(eff. date of

value)

$4.25/Watt

(6 mo. ago)

N/A

Gross Total

$24,000

$19,125

N/A

Rebates

Available

Today

$2,000

$2,000

N/A

Parking

2-Car Gar.

2-Car Gar.

1-Car Gar.

+$3,000

Gross Living

Area

1,600 sq. ft

1,550 sq ft.

1,625 sq. ft

Adjusted

Home Sales

Prices

$220,000

$207,000

Value of PV

System

Comp 1 ($220,000) less Comp 2 $207,000 =

$13,000 value for 4.5 kW system, or $2,888

per kW ($2.89/Watt)

Shading

None

Partial

N/A

Adjustment

for PV System

$2,888 x 1.5

kW (6 kW –

4.5 kW) =

$4,400 rd

6 kW x

$2,888 =

$17,300 rd

Value of Home

with PV

$224,400

$224,300

1 – For educational purposes only, not actual data

Going beyond the radius of comparable properties, the

appraiser found a PV system located 2 miles away using an

aerial image search, which is available in many mapping

programs available on the internet. After determining that

address, the appraiser checked to see if the permit was pulled

and found that the same company installed this system. This

home had not sold; however, the appraiser wanted to know if

any other PV systems were nearby to help understand the

market. The appraiser then contacted the installer and found

out that the 4.5 kW PV system, located close to the property

for sale was purchased by the homeowner, and the one 2 miles

away was a newer 6 kW PV system, but owned by a third-

party. From that information, the appraiser was able to

understand there is some demand for PV systems in this area

with different ownership options.

B. Analyzing Comparable Sales

The two comparable sales provide good support for a value

of the subject property. Comp 1 deserves most consideration

because it has a PV system; however, it is a smaller system

with some shading that will negatively affect the energy

production. Pairing Comp 1 to Comp 2, a similar house

without a solar PV system, provides good support for the

$2,888 adjustment per kW. The only other adjustment is for

the garage size difference. The adjustment is based on market

extraction. After adjustments are applied, the two sales closely

support a value conclusion at $224,400 for the value of the

home. Using the $2,888/kW the value of the PV system is

$17,328.

C. Analyzing the Cost Approach

The appraiser has enough information to apply the physical

age-life method in the cost approach. Table 1 shows the cost

to install that same system today, the effective date of the

appraised value. The appraiser finds out that the PV panels

have a 25-year warranty and the inverter has a 10-year

warranty. Assuming the useful lifetime of 25 years, the

appraiser develops potential contributory values, showing the

depreciation of the PV system and the gross and net costs

(Table 3). Comp 1 and Comp 2 are not used in this analysis.

TABLE 3

AGE-LIFE DEPRECIATION – 6 KW PV SYSTEM

Useful Life

25 yrs

Age

5 yrs

Physical Depreciation %

20%

6 kW Gross Installed Cost today

$24,000

6 kW Net Installed Cost today

$15,400

Gross Cost Today - Depreciation Amount

$4080

Net Cost Today - Depreciation Amount

$3080

Final Gross Depreciated Value

$19,200

a

Final Net Depreciated Value

$12,320

a – value does not include obsolescence due to superadequacy.

As discussed above, when looking at the net value, the tax

situation is very different between owners and years; in the

year it was purchased, there was a federal tax credit, however

it was capped at $2,000 and for this system the tax credit was

only able to reduce the price paid by $2,000, from $42,000 to

$40,000, with a resulting net depreciated value of $12,320. A

new system now costs less than it did 5 years ago, and the

amount of tax credit available today is greater. However, that

tax credit is not available to seller if the entire system had to

be replaced. The gross depreciated value would be more

applicable here with an amount showing less than the cost of

purchasing a new system, however there is more to this

approach than just depreciation.

A challenge with using this approach exclusively is that it

does not consider potential obsolescence that may exist due to

superadequacy. In other words, the market is not willing to

pay full gross cost. For instance, a swimming pool on a brand

new house costs $35,000 and one year later the owners sold

the house. Upon the sale of this one-year old house it sold for

only $10,000 more than the same house without a pool. The

difference between the $35,000 one year ago and $10,000 on

resale is due mainly to obsolescence due to a superadequacy.

Only a small amount of the $15,000 in loss is attributed to the

physical depreciation. (Physical age/life method provides

physical depreciation and does not consider obsolescence.)

To get a better understanding of how this cost approach

value may fit with the other methods, it should be compared to

the value developed using an income approach, which

considers the geographic variability of energy produced and

price paid for the energy.

D. Analyzing the Income Approach – Discounted Cash Flow

The appraiser was able to gather the necessary information

from the homeowner to populate the solar PV section in AI

Form 820.04 and from there, was able to utilize the PV

Value® tool to develop an income approach to value. The

appraiser did not have access to utility savings information

before or after the PV system was installed or information

about rents paid in the vicinity of the subject property and

determined the gross rent multiplier method would not be

appropriate. The information about the PV system is presented

below in Table 4 along with the results of the DCF analysis

using PV Value®.

TABLE 4

DISCOUNTED CASH FLOW – 6 KW PV SYSTEM

System Size

6 kW

System Age

5 yrs

Remaining Energy

20 yrs

Derate

0.77

Degradation Rate

20%

Array Type

fixed

Array Tilt

latitude

Array Azimuth

180

30-year fixed 60 day Conv.

3.51

Avg. Discount rate (50-200 bp spread)

4.76

Utility Rate

11.50 c/kWh

Utility Escalation Rate

1 %

O&M Expenses

55 c/Watt

Annual PV Production –

start year 6

9975 kWh

Avg. appraisal range of value estimate

$13,800

The result here indicates that based on all of these unique

characteristics that are a function of the location of the PV

system and energy it produces, the value estimate is $13,800.

If this system were shaded, then the derate value could be

changed, as shading is included in the PVWatts® derate

definition. This approach gives the knowledgeable appraiser a

number of options to develop value in light of many aspects

that reduce the optimal energy output from the PV system.

If the appraiser had more detailed information about the PV

system on Comp 1, PV Value® could be utilized to better

understand the income value for that PV system, and make

adjustments accordingly. This information could be made

available from the installer, if the appraiser was able to

determine the installation company from the filed permit, or it

may eventually be in the MLS system, as the example here

stated that the MLS in this location just started adding fields

that can help capture the inputs for developing value using a

discounted cash flow analysis.

E. Reconciliation

At this stage, the appraiser will consider all approaches used

to estimate value. The strengths and weaknesses of each

approach are carefully weighed to form an opinion of the

value of the PV system. The appraiser considers data available

to support each of the steps and reliability of the data sources.

Whether the market will support any of these estimates is a

large part of what value the appraiser will determine. An

underwriter may choose to remove the value from the

equation but cannot force an appraiser to remove value

without accepting a value subject to a hypothetical condition

that the PV system has no value when in fact the appraiser

determined that it does.

In reconciling the sales comparison approach, Table 5 gives

an idea of the values the appraiser will consider when

developing the value. The two comparable sales provide good

support for a value of the subject property. Using the

$2,888/kW from Table 3, the value of the PV system is

$17,328. Currently, in most markets comparable properties

that have sold with PV systems may be non-existent, and

relying exclusively on this approach may not accurately reflect

market demand for the income producing benefits of a PV

system.

The cost approach was only applied to the subject property

and done to show the limitations of this approach due to the

need to better understand obsolescence due to superadequacy,

which for PV systems is essentially due to the gross price not

being paid due to the presence of incentives. Currently in most

all markets in the U.S., these incentives are still important in

attracting new market participants.

If the appraiser determines this market supports PV systems

based on willingness from the buyer in this transaction, or

other studies available in the subject area, the appraiser may

reconcile more closely to the Income Approach indication. It

is important to note however that the current installed cost sets

the upper limit of value. It is usually less reliable for PV

systems because of its uniqueness in the market leaving the

depreciation estimate less reliable. Also, the partial shading in

the comparable property example makes it difficult to

understand the percentage reduction in energy production. For

this example, in a supportive market with a knowledgeable

and willing buyer and seller that understand the income

benefits provided by a PV system, the income approach makes

more sense and has more support for the conclusion.

TABLE 5

RECONCILIATION

Sales Comparison

$17,328

Cost Approach

a

$19,200

Income DCF

$13,800

a – physical depreciation only, could be much less if

obsolescence due to super adequacy is included

VI. STANDARD DOCUMENTATION

Based on the example appraisal presented above, the

potential lack of documentation available to an appraiser can

be a challenge. An area that is currently lacking any standard

approach is the concept of how a PV system’s characteristics

are documented, what is being collected, by whom, and where

can the data reside in a way that can streamline the home sales

process.

This process is more commonplace for commercial PV

systems that undergo a commissioning process as there is a

benchmark for comparison to meet conditions in a

performance guarantee, or if the system has to be repaired

[16]. Many states and municipalities collect PV system data as

part of incentive program applications, though as incentive

programs start phasing out, the only places to find data will

include the PV system installers as well as local building

permit databases. Trying to track down this data could prove

time consuming and a hindrance for an appraiser developing

an accurate value estimate.

This problem could be remedied if PV system data is

readily available, either at the property or from when the

house is listed in the local multiple listing service (MLS).

If the data is available at the property, there could be a way

to provide permanent documentation similar to what NEC 690

or the IAPMO Uniform Solar Energy Code requires for

disconnect labeling. For example, the Public Service

Company of New Mexico requires a weatherproof and easily

accessible location for a one-line diagram and site map.

Currently, PV systems in the U.S. are not required to have this

data easily accessible, though if the homeowner no longer can

find the PV system paperwork, having it permanently located

near the PV system interconnection point would help an

appraiser determine the PV system characteristics.

Using the MLS, a real estate agent can capture PV system

data during a home sale as the fields (if available in the MLS)

will be available for the listing agent to fill out with

information provided by the homeowner. Having the MLS

fields populated has the added benefit of giving appraisers

additional data points for determining where PV may exist,

especially when conducting a comparable sales analysis.

There are multiple challenges with setting up an MLS to

capture this information, though there is work that is focusing

on this effort to include solar as well as energy efficient

features [17].

Another effort being made to collect PV system data either

before or during an appraisal is to fill out the AI Residential

Green & Energy Efficiency Addendum, which helps support

the valuation of features that are not included on the Uniform

Residential Appraisal Report (URAR) Form 1004 required by

Fannie Mae. The Appraisal Institute created AI Form 820.04

to capture the necessary information to develop an estimate of

value for solar PV systems [15]. Home builders and real estate

agents can also fill out this form and give to assist the

appraiser. A database application that can capture the

information filled out on this form and make it available to

appraisers and real estate agents would be one way to make

PV system information more readily available to help

facilitate real estate transactions with PV systems.

VII. LINK BETWEEN PV MARKET VALUE AND FINANCING

If there are lower cost financing products available to

purchase a home, why are low rates not available to

prospective purchasers of PV systems? Consider for example

the long-term trend in mortgage interest rates (30-yr fixed) has

shown a decrease in the past 10 years from around 8% to just

below 4% [18]. Also, home equity is starting to “reappear” in

many homes [19] as home prices nationally appear to be

increasing [20]. Borrowing against the home’s equity provides

access to these lower rates, though even these home equity

rates are not as low as a standard conforming first mortgage.

Part of the challenge is that the price paid for PV systems is

still high, with the national average at $5.04/Watt [21]

equating to approximately $25,200 before incentives or tax

credits for a 5 kW PV system. These additional loan amounts

with modified paybacks that range from a few years to 15

years can be financed through secondary secured and

unsecured loan products with interest rates much higher than

the current conforming loan rates. If home prices continue to

increase and PV system prices decrease, the homeowner will

be better positioned to use the equity in their home to finance

solar with lower rates, and current secondary mortgage and

loan products may respond with lower rates to remain

competitive with home equity refinancing.

The discussion about interest rates available for financing

begs the question about the role of appraisers in helping

homeowner’s access lower interest rates typically available for

first mortgages. Consider a loan product that allows for the

inclusion of a PV system value into the loan to value ratio for

the borrower based on the understanding the PV system will

reduce electricity costs as a function of the market value of the

energy produced.

The SAVE Act [22] has outlined this process for energy

efficiency, however for solar if an as-installed value could be

developed before the solar is installed with current appraisal

approaches, new conventional 1

st

mortgage loan products

could then be developed with lower rates that allow for the

installation of a PV system after the home is purchased or

refinanced. For example, strict risk-based rules would most

likely need to be implemented to protect the interest of both

the lender and borrower such as: 1) escrowing of funds with

bonded escrow agent, 2) approval of bonded and licensed

contractor to install the system, 3) funds should be subject to

normal program LTV guidelines, 4) additional loan payment <

90% of estimated monthly savings from PV energy generation

(proof of positive economic benefit), or percent acceptable to

GSE’s, 5) roof less than 5 years old, or determination that

remaining useful roof life > (reasonable %) useful life of PV

system, and 6) no mortgage funds allowed to monetize

incentives (rebates or tax credits, etc.).

The product discussed above is an example of how access to

lower rates could be achieved specifically for PV systems, and

further dialogue between the GSE’s and the Appraisal industry

would need to take place. In addition, costs would most likely

need to decline further from current levels and value for PV

systems would need to be recognized before these products

could be created and offered to consumers. It is anticipated,

according to lending industry sources, that a minimum of US

$400M per quarter would be required to develop a new

product which based on current average national loan size of

~$230k would translate into ~1,800 new loans per quarter in

demand from interested consumers who want to own and

finance a PV system with the purchase of refinance of their

home. As underwriters begin to accept valuations of PV

systems developed by appraisers then products like this would

be feasible.

VIII. CONCLUSIONS

This paper presents a case for why it is important that

standard appraisal techniques be utilized and accepted for

developing value for PV systems. One of the most pressing

challenges is train appraisers to first understand how PV

systems operate, and concurrently, educate them on certain

techniques that are appropriate for certain markets depending

on how well PV is understood and desired in that community.

This is currently being done with the Appraisal Institute

offering a comprehensive course that covers both residential

and commercial PV system appraisal techniques; though it

will take some time to educate all appraisers on the benefits

and value provided by PV systems.

There are many areas that could help appraisers gather the

necessary data, and as the example appraisal shows, there is

not one central database that appraisers can use that has both

past and current cost information for PV systems in that

market, or has site-specific information on the installation

properties of existing PV systems. As PV systems age,

documentation may be even more difficult to obtain and it is

important that PV systems are captured in real estate multiple

listing databases, or other databases that could be developed

for the benefit of appraisers to help them more efficiently

gather information they need to develop an opinion of value.

As this paper focused primarily on residential topics related to

appraising PV systems, many of these areas of concern and

study also apply to commercial PV systems. The techniques

utilized by commercial appraisers make it technically easier to

value PV systems, as the use of the income and cost

approaches are better understood and readily accepted by

lenders in the realm of income producing properties. To value

PV systems with a recognition of the income producing

aspects that make these systems desirable in many markets in

the U.S., residential appraisers will learn to use these

approaches and develop accurate estimates of value that will

help facilitate real estate transactions with PV systems.

Ultimately, as PV systems increase in popularity and

become more commonplace in most markets in the U.S.,

appraisers will be ready to help facilitate homes sales with PV

systems as they have data more readily available to employ

the proper methods of valuation taught in appraiser education

courses. Supporting the value of a PV system will be more

accurate due to the abundance of market data and that will

result in acceptance by underwriters. Partnerships with the real

estate, appraisal, lending and underwriting industries are just

now beginning to develop, which will help speed up this

process and essentially give appraisers the professional and

technical support needed to develop values for PV systems.

ACKNOWLEDGEMENT

Sandia National Laboratories is a multi-program laboratory

managed and operated by Sandia Corporation, a wholly

owned subsidiary of Lockheed Martin Corporation, for the

U.S. Department of Energy’s National Nuclear Security

Administration under contract DE-AC04-94AL85000.

REFERENCES

[1] U.S. Department of Energy, “SunShot Vision Study,” February

2012.

[2] P. Zhai and E. D. Williams, “Analyzing consumer acceptance of

photovoltaics (PV) using fuzzy logic model,” Renewable

Energy, vol. 41, pp. 350-357, 2012.

[3] Appraisal Standards Board, “Uniform Standards of Professional

Appraisal Practice,” Standard Rule 1-4, 2012-2013 Edition.

Available: www.uspap.org

[4] Appraisal Standards Board, “Uniform Standards of Professional

Appraisal Practice,” Competency Rule, 2012-2013 Edition.

Available: www.uspap.org

[5] Fannie Mae, “Selling Guide, Fannie Mae Single Family,” 2013.

Available:

https://www.fanniemae.com/content/guide/sel011713.pdf

[6] J.R. Webb, “The Influence of Solar Energy Systems on the

Value of Dwellings: Theory Vs. Practice,” The Real Estate

Appraiser and Analyst, pp. 4-6, January – February 1980.

[7] J. Harris, “The Value of Solar Energy: Chic, Patriotism and

Economic Rationality,” The Real Estate Appraiser and Analyst,

pp. 5-7, Fall 1984.

[8] B. Hoen, R. Wiser, P. Cappers, and M. Thayer, “An Analysis of

the Effects of Residential Photovoltaic Energy Systems on

Home Sales Prices in California,” LBNL-4476E, Lawrence

Berkeley National Laboratory, April 2011

[9] Appraisal Institute, “Residential and Commercial Valuation of

Solar,” Instructional Handbook, 2013.

[10] S. K. Adomatis, “Valuing High Performance Houses,” The

Appraisal Journal, pp. 195-201, Spring 2010.

[11] R. Nevin, and G. Watson, “Evidence of Rational Market

Valuations for Home Energy Efficiency,” The Appraisal

Journal, Vol. 68, pp. 401-409, 1998.

[12] M. McCabe, and L. Merry. “The Resale Market Value of

Residential Solar Photovoltaics: A Summary of Literature and

Insight into Current Value Perceptions.” Available:

http://www.costar.com/josre/pdfs/ResaleMarketValueofResident

ialSolarPVfinalfull_McCabe_5-14-10.pdf

[13] J. L. Johnson, and G.T. Klise, “PV Value® User Manual v. 1.1,”

Sandia National Laboratories, SAND2012-7306P, 2012.

Available: http://pv.sandia.gov/pvvalue

[14] G. T. Klise, J. L. Johnson, and S. K. Adomatis, “Establishing

Proper Valuation Techniques for Solar Photovoltaic Systems,”

The Appraisal Journal, In Review.

[15] Appraisal Institute, “Form 820.04: Residential Green and

Energy Efficient Addendum,” Available:

http://www.appraisalinstitute.org/education/green_energy_adde

ndum.aspx

[16] B. Gleason, “PV System Commissioning,” Online article in

SolarPro, Issue 2.6, Oct/Nov 2009. Available:

http://solarprofessional.com/articles/design-installation/pv-

system-commissioning

[17] U.S. DOE, “DOE Transaction Process Roadmap,” Building

Technologies Program, Draft May 2013.

[18] MBA Mortgage Rates (1991 to Present). Available at:

http://www.mortgagenewsdaily.com/mortgage_rates/charts.asp

[19] CoreLogic, Core Logic Q2 Negative Equity Report, 2012.

[20] CoreLogic, CaseShiller Home Price Index, 2013.

[21] SEIA, “U.S. Solar Market Insight 2012 Year in Review,”

Available at: http://www.seia.org/research-resources/us-solar-

market-insight-2012-year-review

[22] Institute for Market Transformation, “SAVE Act,” Available:

http://www.imt.org/finance-and-leasing/save-act