Audit Report

Follow-up: Minor Children

Receiving Social Security Benefits

Without a Representative Payee

A-13-17-50169 | June 2019

MEMORANDUM

Date:

June 6, 2019

Refer To:

To:

The Commissioner

From:

Inspector General

Subject:

Follow-up: Minor Children Receiving Social Security Benefits Without a Representative Payee

(A-13-17-50169)

The attached final report presents the results of the Office of Audit’s review. The objective was

to determine whether the Social Security Administration complied with its policies when it paid

benefits to minor children.

If you wish to discuss the final report, please call me or have your staff contact Rona Lawson,

Assistant Inspector General for Audit, 410-965-9700.

Gail S. Ennis

Attachment

Follow-up: Minor Children Receiving Social Security Benefits

Without a Representative Payee

A-13-17-50169

June 2019 Office of Audit Report Summary

Objective

To determine whether the Social

Security Administration (SSA)

complied with its policies when it paid

benefits to minor children.

Background

The law requires that most minor

children have representative payees to

manage their benefits to ensure the

payments are used for their current and

foreseeable needs.

SSA generally presumes minor

children under age 18 are incapable of

managing their own benefits. As a

result, SSA usually appoints

representative payees to manage the

benefits of children. However, SSA

can pay a child age 15 through

17 directly if the child meets certain

criteria.

We identified 709 minor children

under age 15 and 1,273 minor children

who were between age 15 and 17 and

5 months as of April 2017 that did not

have appointed representative payees.

We provided a list of the 709 minor

children under age 15 to the Agency

for review and corrective action. In

addition, from the group of children

between the ages 15 and 17 and

5 months, we randomly selected 50 for

review.

Findings

SSA did not always comply with its policies when it paid benefits

to minor children. Of the 709 minor children under age 15 we

identified and referred to SSA for review and corrective action,

SSA confirmed it had not appointed representative payees for

668 as of April 2017. We estimate the Agency paid these children

approximately $12.2 million. For the remaining 41 children, SSA

reported appointing representative payees for 22 before our

referrals, suspending or terminating benefits for 14, and correcting

the dates of birth for 5 who were actually over age 18.

Of the 50 children we reviewed who were between ages 15 and

17 and 5 months, SSA did not comply with its policies for 46 who

received benefits. The Agency confirmed it did not appoint

representative payees for 32 child beneficiaries. Based on our

sample, we estimate the Agency paid 815 child beneficiaries

approximately $22.5 million. Additionally, SSA did not document

capability determinations for 14 children it paid directly as is

required by Agency policy. Based on our sample, we estimate SSA

did not properly document capability determinations for

356 children it paid directly.

Recommendations

We recommend SSA:

1. Direct employees to (1) comply with policies for appointing

representative payees for minor children, (2) document

capability determinations, and (3) adjudicate representative

payee applications properly.

2. Implement a process to periodically identify all children under

age 17 and 5 months being paid directly; and determine and

document whether the Agency needs to appoint representative

payees.

SSA agreed with our recommendations.

Agency Actions Resulting from the Audit

In response to our audit, SSA appointed representative payees for

the children who were still receiving benefits and needed to be

served by representative payees.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169)

TABLE OF CONTENTS

Objective ..........................................................................................................................................1

Background ......................................................................................................................................1

Results of Review ............................................................................................................................4

Minor Children Under Age 15 ...................................................................................................4

Children Receiving Benefits Without Representative Payees .............................................5

Benefits Received by Individuals Who Were Not Representative Payees ..........................7

Prior Audit ...........................................................................................................................7

Minor Children Age 15 and Older .............................................................................................8

Children Receiving Benefits Without Representative Payees .............................................8

Capability Determination Policy for Children ...................................................................10

Prior Audit .........................................................................................................................11

Conclusions ....................................................................................................................................11

Recommendations ..........................................................................................................................12

Agency Comments .........................................................................................................................12

Agency Actions Resulting from the Audit .....................................................................................12

– ................ A-1

– Scope and Methodology ..................................................................................... B-1

– Sampling Methodology and Results ................................................................... C-1

– Agency Comments .............................................................................................. D-1

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169)

ABBREVIATIONS

C.F.R. Code of Federal Regulations

eRPS Electronic Representative Payee System

Form SSA-11-BK Request To Be Selected As Payee

OASDI Old-Age, Survivors and Disability Insurance

OIG Office of the Inspector General

POMS Program Operations Manual System

SSA Social Security Administration

SSI Supplemental Security Income

U.S.C. United States Code

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 1

OBJECTIVE

Our objective was to determine whether the Social Security Administration (SSA) complied with

its policies when it paid benefits to minor children.

BACKGROUND

Some individuals cannot manage or direct the management of their finances because of their

youth or mental and/or physical impairments. For such beneficiaries, Congress provided for

payment through representative payees who receive and manage benefits for the beneficiaries.

1

A representative payee may be an individual or an organization.

2

SSA selects representative

payees for Old-Age, Survivors and Disability Insurance (OASDI)

3

and Supplemental Security

Income (SSI)

4

beneficiaries

5

when representative payments would serve the beneficiaries’

interests. Approximately 5.8 million payees manage $70 billion in annual benefits for

8.1 million beneficiaries. Fifty-three percent of the beneficiaries are minor children.

6

The law requires that most minor children have representative payees to manage their benefits to

ensure they are used for the children’s current and foreseeable needs.

7

Therefore, SSA generally

presumes minors under age 18 are incapable of managing their own benefits. SSA policy

8

states

a child under age 15 must have a representative payee unless the child is emancipated under

State law. As a result, SSA usually appoints a representative payee to manage a child’s benefits.

1

Social Security Act, 42 U.S.C. §§ 405(j)(1), 1383(a)(2)(A)(ii) (govinfo.gov 2017). See also 20 C.F.R.

§§ 404.2001(b), 416.601(b) (govinfo.gov 2016).

2

20 C.F.R. §§ 404.2001(a), 416.601(a) (govinfo.gov 2016).

3

The OASDI program provides retirement and disability benefits to qualified individuals and their dependents as

well as to survivors of insured workers. See Social Security Act, 42 U.S.C. §§ 402, 423 (govinfo.gov 2017).

4

The SSI program provides payments to individuals who have limited income and resources and are age 65 or older,

blind, or disabled. Social Security Act, 42 U.S.C. § 1381 (govinfo.gov 2017). See also 20 C.F.R. § 416.110

(govinfo.gov 2018).

5

Throughout this report, we use the term “beneficiary” to refer to OASDI beneficiaries and SSI recipients, and the

term “benefits” to refer to OASDI benefits as well as SSI payments.

6

SSA, Annual Report on the Results of Periodic Representative Payee Site Reviews and Other Reviews, p.2 (2018).

7

20 C.F.R. § 416.601-610 (govinfo.gov 2016).

8

SSA, POMS, GN 00502.001, C (January 26, 2017).

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 2

However, SSA can pay a child age 15 through 17 directly if the child

is emancipated,

is entitled to disability benefits based on his/her own earnings,

is on active duty in the armed forces,

is living alone and self-supporting,

is a parent and filed for his/her own or his/her child’s benefits and has experience handling

finances,

is within 7 months of attaining age 18, or

has demonstrated the ability to handle his/her finances.

9

Additionally, if SSA determines a child is capable of receiving his/her benefits without a

representative payee,

10

Agency staff must document the results of its capability determination in

the Electronic Representative Payee System (eRPS) or on a Report of Contact if they cannot do

so in eRPS.

11

However, a beneficiary age 15 to 18 can be paid directly on an interim basis even if he/she is

incapable of managing benefits.

12

In these instances, the Agency takes a Form SSA-11-BK,

Request To Be Selected As Payee (SSA 11-BK) and completes follow ups with the beneficiary

every 90 days to ensure the benefits are being used properly.

13

SSA can decide to continue direct

payment permanently if it appears the beneficiary is using the money to meet his/her needs and

no other suitable payee has been found.

14

Representative payees have many responsibilities, including determining beneficiaries’ current

and foreseeable needs; using Social Security benefits in the beneficiaries’ best interest; and

keeping detailed and accurate records of how the payments are used to provide an accurate report

to SSA, if requested.

15

9

SSA, POMS, GN 00502.070, A.1 (January 26, 2017).

10

See Footnote 10.

11

SSA, POMS, GN 00502.065, C (June 29, 2017).

12

SSA, POMS, GN 00504.105, A.2 (July 19, 2017).

13

SSA, POMS, GN 00504.105, B.2 (July 19, 2017).

14

See Footnote 14.

15

SSA, POMS, GN 00502.114, A (February 27, 2014).

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 3

SSA replaced the Representative Payee System with eRPS in April 2016 to streamline the

actions and processes for representative payee selections, accounting, and misuse

determinations.

16

The eRPS is intended to help the Agency fulfill its legal duty

17

to investigate

representative payee applicants to determine whether their appointments are in the beneficiaries’

best interests by providing known information about the applicants so SSA can make well-

informed decisions.

18

Further, SSA initiated its automated Sweeper process in December 2017, after it implemented

eRPS. Sweeper reviews applications pending in eRPS and takes action based on case criteria.

Sweeper activates or terminates the appointment of representative payees and closes pending

payee applications in eRPS or identifies necessary actions for pending applications it cannot

automatically clear.

19

SSA staff indicated the Agency used Sweeper monthly.

This review is a followup to our May 2011 report, which stated SSA did not always appoint

representative payees for children under age 15 in accordance with its policies.

20

In addition,

SSA did not comply with its policies and procedures for children age 15 to 17 who managed

their own benefits. Our report included five recommendations, which SSA generally agreed to

implement. See Appendix A for a summary of the prior report.

We identified 1,982 children who were receiving benefits as of April 2017 but did not have

representative payees appointed or were themselves listed as their own representative payees on

their records. Of these, 709 were under age 15, and 1,273 were between age 15 and 17 and

5 months.

21

We referred the 709 children under age 15 to the Agency for review and corrective

action. In addition, we randomly selected 50 children who were between age 15 to 17 and

5 months for review. See Appendix B for our scope and methodology and Appendix C for our

sampling methodology and results.

16

SSA, eRPS – Representative Payee Redesign, ssa.gov (last visited February 5, 2019).

17

Social Security Act, 42 U.S.C. § 405(j)(2)(A)(i) (govinfo.gov 2017).

18

SSA, POMS, GN 00502.120, A (April 15, 2016).

19

SSA, MSS Messages, Electronic Representative Payee System (eRPS) – Maintenance Release Enhancement,

MSS17-146 eRPS (December 14, 2017).

20

SSA, OIG, Minor Children Receiving Benefits Without a Representative Payee, A-13-10-10104 (May 2011).

21

SSA may directly pay children within 7 months of attaining age 18.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 4

RESULTS OF REVIEW

We found instances where SSA did not comply with its policies when it paid benefits to minor

children. As of April 2017, the Agency had not appointed representative payees for

668 children

22

under age 15. We estimate SSA paid these children approximately $12.2 million

even though they did not have representative payees.

23

Of the 1,273 children age 15 through 17 and 5 months,

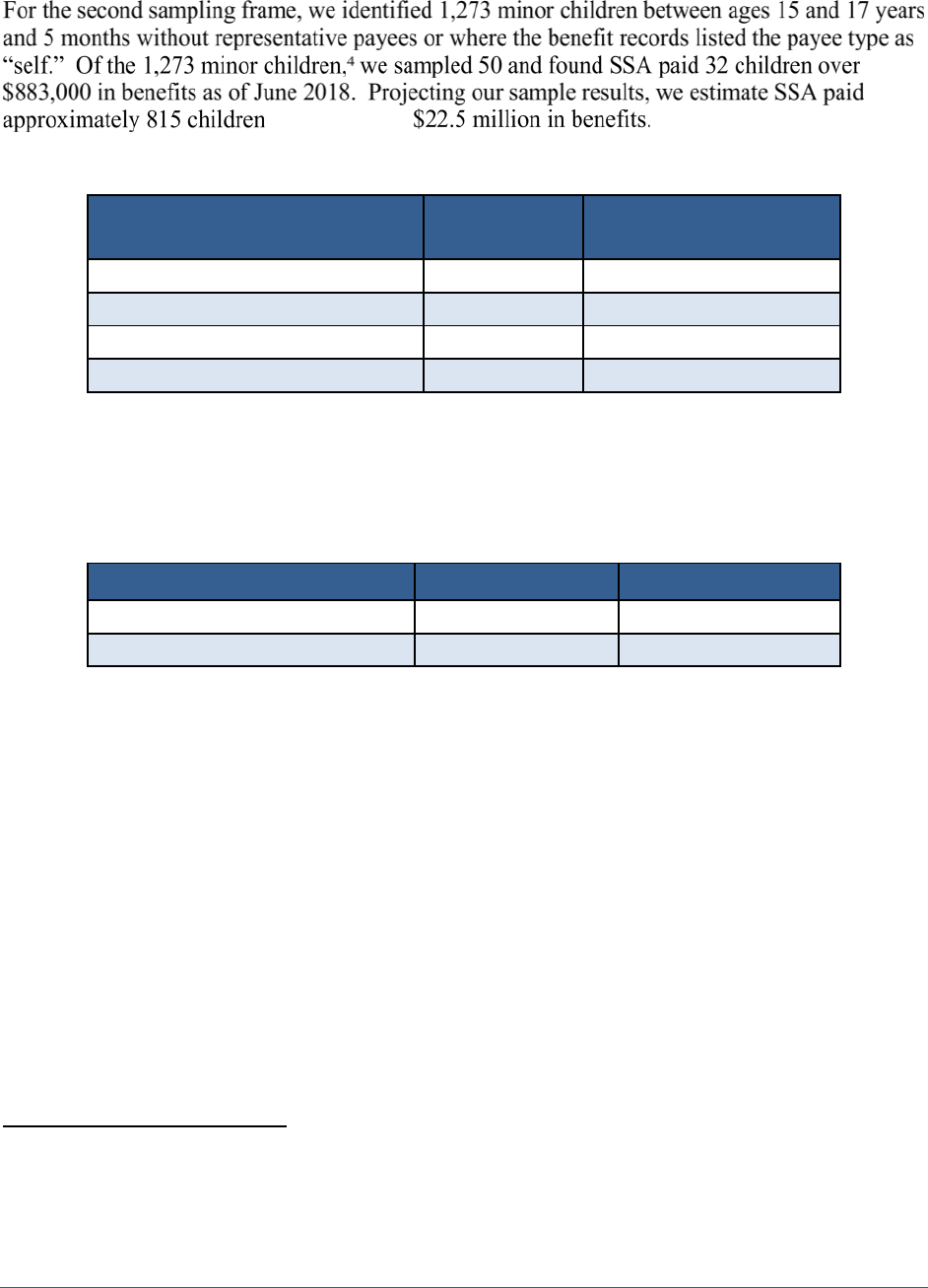

24

we estimate SSA paid 815

approximately $22.5 million although there were no representative payees on the children’s

records. In addition, we estimate SSA did not properly document capability determinations for

356 children it paid directly.

Minor Children Under Age 15

Of the 709 minor children under age 15 we identified and referred to SSA for review and

corrective action, SSA confirmed it had not appointed representative payees for 668 as of

April 2017.

25

We estimate the Agency paid these children approximately $12.2 million without

representative payees.

26

For the remaining 41 children, SSA appointed representative payees for

22 before our referrals,

27

suspended or terminated benefits for 14, and corrected the dates of birth

for 5 who were actually over age 18.

Furthermore, the Agency provided additional information that indicated instances where

individuals other than the minor children may have received the benefits. Using information and

an analysis method SSA provided, we identified 118 instances, from the 668 records, where

individuals other than the minor children received the children’s benefits. However, coding on

the children’s benefit records did not indicate the children had representative payees. Benefit

record coding shows when SSA appointed the representative payee and the relationship between

the beneficiary and the representative payee. Additionally, the coding allows the Agency to

22

Of the 668 children, we identified 3 during our 2011 audit.

23

Estimated payments cover the following periods: (a) from the time SSA began payments to when SSA appointed

representative payees or (b) from when SSA began payments to June 2018.

24

We found six children from our 2011 audit included in this group of minor children.

25

As of March 2019, SSA had appointed representative payees for 659 children, and 9 children had been suspended

and did not have a representative payee. For children with suspended benefits, SSA should appoint a representative

payee if a child returns to current pay status.

26

See Footnote 24.

27

The 22 children were included in our April 2017 data extract. SSA appointed representative payees for these

children between the date of our extract and the date we referred the 709 children to the Agency.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 5

know whether the representative payee has custody of the beneficiary and determine when SSA

needs to send a representative payee accounting form.

28

,

29

Children Receiving Benefits Without Representative Payees

To determine why SSA paid children under age 15 without appointing representative payees, we

requested the Agency review the 709 cases we identified. SSA confirmed it did not appoint

representative payees for 668 children but should have. The Agency paid the 668 children

approximately $309,000 each month. According to SSA staff, the Agency did not appoint

representative payees for 518 children because of information systems errors,

30

140 children

because of employee processing errors, and 10 children for unknown reasons.

Information Systems Errors

Of the 668 children, the Agency’s review indicated it paid 518 without representative payees

because of information systems errors. SSA paid the children approximately $241,000 each

month.

For 454, representative payee application errors occurred before SSA implemented eRPS.

31

For 61, representative payees were erroneously removed from the children’s benefit records.

For three, eRPS did not properly process representative payee applications.

For example, the father of a 5-year-old beneficiary applied to serve as representative payee in

July 2015, before SSA implemented eRPS. However, because of issues with the Representative

Payee System (the predecessor to eRPS), the Agency did not process the representative payee

application. As a result, SSA issued monthly benefits of $313 to the child. The Agency

appointed the child’s grandmother as representative payee in December 2017.

In another instance, SSA reported a systems error inadvertently removed the representative

payee from an 8-year-old beneficiary’s record. When SSA staff changed the child’s name on the

Numident, staff did not complete a subsequent change to the child’s benefit record. Therefore,

the name change did not synchronize with the child’s eRPS record, which no longer included the

child’s representative payee. The Agency took corrective action and selected the child’s mother

as representative payee.

28

The accounting report is used to monitor how the representative payee spent or saved the benefits on the

beneficiary’s behalf, identify situations where representative payment may no longer be appropriate, or determine

whether the representative payee is no longer suitable.

29

SSA, POMS, GN 00605.020, B (April 15, 2016). This policy was in effect during our audit period. SSA updated

its policy on March 13, 2019.

30

Of the 518 children, 3 were included in our prior audit.

31

Of the 454 children, 3 were included in our prior audit.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 6

In a third instance, SSA approved a benefit claim for an 11-year-old beneficiary in 2016.

According to SSA, the representative payee application recorded in eRPS became “stuck” in

“ready to process” status, and Agency staff subsequently closed the application. To correct the

problem, SSA entered a new representative payee application and selected a representative payee

in eRPS in October 2017.

SSA Employee Processing Errors

SSA explained for 140 children, to whom it paid approximately $64,000 each month, Agency

employees did not always take representative payee applications, select representative payees, or

input the information correctly into SSA’s information systems, as required. This included

63 children for whom SSA did not select representative payees,

41 children for whom SSA did not take representative payee applications, and

36 children for whom SSA improperly coded information in its systems.

For example, the Agency completed a representative payee application for a 9-year-old

beneficiary but did not select and add the representative payee to the child’s benefit claim. SSA

processed the child’s claim and issued benefits without placing the representative payee on the

benefit record.

In another instance, SSA did not take a representative payee application when it completed a

benefit claim for a 5-year-old beneficiary. The Agency paid benefits directly to the child from

June 2013 to January 2018, when SSA appointed the child’s mother as representative payee.

In a third example, in October 2016, the Agency manually processed a benefit claim for a 4-year-

old beneficiary and took a representative payee application for the child’s mother in eRPS. The

representative payee information was not properly coded during manual processing. This coding

problem caused SSA to issue benefits to the child without establishing a representative payee.

The Agency added the representative payee to the child’s benefit record in November 2017.

Unknown Problems

SSA could not determine why it paid 10 children approximately $4,000 each month without

representative payees on their records. In one instance, SSA paid a 1-year-old beneficiary

directly. SSA did not explain how this occurred, but Agency staff did appoint the child’s mother

as her representative payee in July 2017.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 7

Benefits Received by Individuals Who Were Not Representative Payees

SSA provided information that indicated situations where individuals other than the minor

children may have received the children’s benefits. Using information and an analysis method

SSA provided, we re-examined information for the 668 children and identified 118 instances

involving individuals other than the children receiving benefits. For the 118 children, we found

the following.

In 101 instances, SSA had representative payee applications for children before we referred

the records to the Agency for review and corrective action. However, SSA did not fully

process the applications, the representative payees no longer appeared on the records, or we

could not determine why representative payees were not on the children’s benefit records. In

one instance, the Agency obtained a representative payee application for someone other than

the person who received the minor child’s benefit.

In 17 instances, SSA did not obtain representative payee applications.

For example, in June 2015, SSA did not select a woman who applied to be representative payee

for her 11-year-old child; however, the Agency sent her the child’s benefits. After our referral,

SSA selected the child’s mother as representative payee in July 2018.

In another instance, the Agency began the application process for a 10-year-old child’s

representative payee after we referred information for its review. The individual, whom SSA

selected as the child’s representative payee in January 2018, received benefits before SSA took

her application to serve as the child’s representative payee.

Additionally, for 6 of the 118 children, the Agency appointed representative payees who were

not the individuals receiving the children’s benefits. For example, an individual applied in

August 2015 to be representative payee for a 2-year-old child; however, the application was

“stuck” in eRPS. As a result, the individual continued receiving the child’s benefits although the

Agency did not officially select the person as the child’s representative payee. After our referral,

in February 2018, SSA appointed a social agency to serve as the child’s representative payee.

Prior Audit

Our prior audit

32

found SSA did not always appoint representative payees for children under

age 15. We found SSA paid children who did not have representative payees on their records.

We provided the Agency a list of 1,351 children under age 15 without representative payees for

review and corrective action. During our current review, we identified three children from the

prior audit, still under age 15, whom SSA continued paying without representative payees on

their records. We requested SSA review the three cases and take appropriate corrective action.

As of June 2018, the Agency had appointed representative payees for all three children. SSA

had paid these children approximately $89,000 since our prior audit.

32

See Footnote 21.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 8

Minor Children Age 15 and Older

We selected a random sample of 50 children age 15 through 17 and 5 months to review. Of the

50 children, SSA paid 4 in compliance with policy. However, SSA did not comply with its

policies when it paid 46 children who did not have representative payees.

SSA determined 32 children

33

were incapable of managing their own benefits but still issued

them benefits without representative payees on their records.

34

SSA did not properly document, in accordance with policies and procedures, its capability

determinations for 14 children it paid directly.

Based on our sample results, we estimate SSA paid 815 children between ages 15 and 17 and

5 months approximately $22.5 million without representative payees.

35

In addition, we estimate

SSA did not properly document capability determinations for 356 children it paid directly.

Children Receiving Benefits Without Representative Payees

Of the 46 children for whom SSA did not comply with its representative payee policies, the

following 32 included instances where the Agency did not appoint representative payees for

child beneficiaries:

27 involved Agency staff initiating representative payee applications but not processing them

properly;

3 involved systems errors; and

2 involved undocumented parents

36

who wanted to act as representative payees, but SSA did

not complete the representative payee applications.

The Agency paid the 32 children over $883,000 before it appointed representative payees for

them or they turned 18.

37

33

SSA can pay the child directly if the child files his/her own initial claim and a representative payee is not available

when the claim is ready to be processed. However, this exception did not apply to any of the 32 children. See SSA,

POMS, GN 00504.105, A, B.2 (July 19, 2017).

34

We found six children identified in our prior audit whom SSA continued paying without representative payees on

their records.

35

Our sample projection is based on 32 children for whom SSA did not appoint representative payees. See

Appendix C.

36

SSA considers an individual undocumented if he/she cannot provide proof of a lawful presence in the United

States.

37

As of June 2018, of the 32 children, 18 had representative payees appointed, 7 had reached age 18, 6 had their

benefits terminated because they were no longer eligible for benefits, and 1 had his/her benefits suspended for

failing to provide required information to SSA.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 9

Representative Payee Applications Not Processed Properly

Of the 32 children, SSA obtained representative payee applications for 27 but did not process

them properly. According to SSA policy,

38

Agency staff is to administer

39

representative payee

applications in eRPS. For 23 of 27 beneficiaries, SSA did not finish processing representative

payee applications, and the children’s eRPS and/or benefit records did not identify representative

payees. In the remaining four instances, SSA failed to include, as required by the procedures for

manually processing applications, copies of documentation in its automated systems. In 2016,

after SSA stopped using its Representative Payee System and began using eRPS, Agency

technicians did not always follow up on representative payee applications that were in process in

the Representative Payee System.

For example, SSA took a representative payee application in May 2013 for a 15-year-old

beneficiary but did not select the representative payee; therefore, there was no representative

payee on the child’s benefit record. In October 2017, we informed SSA of our review results. In

January 2018, the Agency selected a representative payee for this child.

In another instance, when the Agency attempted to contact a 15-year-old recipient to conduct a

redetermination

40

of the child’s eligibility for benefits, SSA received no response. As of

May 2017, SSA had suspended the child’s benefits. As of June 2018, the child was in non-pay

status.

Additionally, we found two instances where individuals other than the children received benefits.

However, SSA did not select representative payees or record them on the children’s benefit

records. According to Agency staff, “. . . the payments were made to the natural mother.” For

these instances, SSA reported that both were the result of coding errors.

System Errors

SSA paid three children who did not have representative payees because of information system

errors. In one instance, in September 2015, SSA’s information systems removed a 16-year-old

beneficiary’s representative payee. SSA appointed a representative payee for this child in

March 2018.

38

SSA, POMS, GN 00502.110, A, B (November 2, 2016).

39

SSA staff uses eRPS to create new representative payee applications and update pending applications.

40

A change in a person’s income, resources, and/or household composition can affect a person’s eligibility for

benefits and the amount of benefits. The law requires that SSA periodically re-determine an individual’s continuing

eligibility to receive benefits and the amount of benefits.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 10

Representative Payee Applications for Undocumented Parents

There were two instances where Agency staff did not include SSA-11-BKs in the Certified

Electronic Folder. According to SSA policy,

41

Agency staff can appoint undocumented parents

as representative payees. However, eRPS does not accept representative payee applications

without a Social Security number, which serves as the unique identifier in the system. Therefore,

when an undocumented parent wants to serve as a representative payee, the individual must

complete an SSA-11-BK, and the Agency should scan the document into the Non-disability

Repository for Evidentiary Documents system or the Electronic Disability system.

42

The two

SSI recipients we identified had undocumented parents who wanted to serve as representative

payees; however, SSA did not retain the SSA-11-BKs of the undocumented parents in the

Certified Electronic Folder.

The Agency reviewed these two instances and agreed with our conclusion. SSA could not locate

the representative payee applications in its systems for the children’s undocumented parents.

However, we confirmed SSA had appointed representative payees for both children as of

June 2018.

Capability Determination Policy for Children

Generally, SSA is required to make capability determinations regarding whether children ages

15 to 17 can manage their own benefits.

43

The Agency directly pays these children if they meet

certain conditions. According to SSA, staff must make a capability determination based on

legal, medical, or lay evidence. Further, Agency staff must properly document the capability

determination, which includes a concluding statement summarizing the facts considered and the

basis for the determination in eRPS.

SSA staff did not document the children’s capability in accordance with its policies and

procedures. SSA decided to pay benefits to 14 children directly, but staff did not properly

document the capability determination. According to SSA staff, employees intended to pay

benefits to these children directly. The Agency considered these children capable of managing

their own benefits and decided not to develop the children’s records any further.

As of June 2018, we had found

six instances where SSA assumed the child was capable of managing his/her own benefits,

six instances where SSA terminated benefits, and

two instances where the child reached age 18.

41

SSA, POMS, GN 00502.117, A.1.a (June 23, 2017). This policy was in effect during our audit period. SSA

updated its policy on March 30, 2019.

42

SSA, POMS, GN 00502.190, B.1 (November 8, 2018).

43

See Footnote 10.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 11

Prior Audit

During our current review, we identified six children

44

age 15 and older from the prior audit

whom SSA continued to pay without representative payees on their records. We requested SSA

review these instances and take corrective action, as appropriate. SSA confirmed five children

did not have representative payees, and one child was age 18. As of March 2019,

in two instances, SSA appointed a representative payee;

in two instances, SSA continued paying benefits to an individual other than the child (“the

natural mother”) because the children’s records were not coded properly;

in one instance, the beneficiary attained at least age 18; and

in one instance, SSA terminated the child’s benefits.

SSA had paid these children approximately $247,000

45

since we completed our prior audit.

CONCLUSIONS

Similar to our prior audit, we found instances where SSA did not comply with its policies when

it paid benefits to minor children without representative payees. Since our prior review, the

Agency had taken some corrective actions; however, we continued to identify problematic

instances similar to those found in our prior audit. Specifically, the Agency did not appoint

representative payees for 668 children under age 15, as required. We estimate SSA paid these

children approximately $12.2 million without representative payees. The 668 children included

3 from our prior audit.

Our review of a sample of children ages 15 through 17 and 5 months found the Agency did not

appoint representative payees for 32 children in accordance with SSA’s policies and procedures.

Based on our sample results, we estimate SSA paid 815 children approximately $22.5 million

without representative payees. In addition, we estimate SSA did not properly document

capability determinations for 356 children it paid directly. We also found six children from the

prior audit included in this group of minor children and determined the status of Agency actions

as of March 2019.

44

The six children were under age 15 at the time of our 2011 audit report and referred to SSA for review.

45

Of the approximate $247,000 paid to these children from the prior audit, as of March 18, 2019, approximately

$77,000 was paid to the two children until representative payees were appointed, approximately $87,000 was paid to

the two individuals receiving payments other than the child, approximately $24,000 was paid to the one child until

the child reached age 18, and approximately $59,000 was paid to the remaining child until the child’s benefits were

terminated.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) 12

RECOMMENDATIONS

We recommend SSA:

1. Direct employees to (1) comply with policies for appointing representative payees for minor

children, (2) document capability determinations, and (3) adjudicate representative payee

applications properly.

2. Implement a process to periodically identify all children under age 17 and 5 months being

paid directly; and determine and document whether the Agency needs to appoint

representative payees.

AGENCY COMMENTS

SSA agreed with our recommendations. The Agency’s comments are included in Appendix D.

AGENCY ACTIONS RESULTING FROM THE AUDIT

In response to our audit, SSA appointed representative payees for the children who were still

receiving benefits and needed to be served by representative payees.

Rona Lawson

Assistant Inspector General for Audit

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169)

APPENDICES

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) A-1

–

In May 2011, we issued a report on Minor Children Receiving Benefits Without a Representative

Payee.

1

Our objective was to determine whether the Social Security Administration (SSA)

appointed representative payees for minor children in accordance with its policies.

Findings and Recommendations

SSA did not always appoint representative payees for minor children in accordance with its

policies. We estimated the Agency did not appoint representative payees, as required, for

approximately 3,200 children under age 18 who had received approximately $66.2 million in

benefits. Since these children did not have representative payees, the Agency was not able to

monitor how the benefits were spent. The majority of the problems were due to employee

processing errors.

We made five recommendations to address our findings, and the Agency generally agreed with

each. Below are our recommendations and actions SSA took to address each.

1. Remind employees to follow policies and procedures when issuing direct payments to

children under age 18. Specifically, (1) appoint representative payees for all children under

age 15 and (2) document capability determinations for children ages 15 through 17 who are

deemed capable of receiving direct payment.

Agency Response: The Agency published an Administrative Message

2

to remind employees

to appoint a payee for children under age 15 and to document capability for children ages

15 to 17 on June 17, 2011.

2. Follow up on the 14 children under age 15 whose benefit payments were suspended pending

appointment of payees and determine whether any of the cases should be referred to our

Office of Investigations for further action.

Agency Response: SSA reported that all regions had taken action to develop and document

cases in their jurisdiction regarding the 14 children under age 15 whose benefits were

suspended. The Agency also indicated representative payee selections, suspensions, and

referrals were made accordingly. We confirmed SSA appointed representative payees for

11 children, but the Agency later terminated benefits for 8 with only 3 children still receiving

benefits as of September 2018. Of the 14, as of September 2018, 9 children were 18 or older

and therefore no longer required representative payees because they were no longer minor

1

SSA, OIG, Minor Children Receiving Benefits Without a Representative Payee, (A-13-10-10104), (May 2011).

2

SSA, AM-11071, Issuing Direct Payment to Children and Documenting Capability-Reminders, (June 17, 2011).

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) A-2

children. Additionally, SSA referred five cases to the Office of Investigations, which found

the allegations did not meet case opening guidelines.

3. Identify pending representative payee applications for children under age 15 before

completing [Representative Payee System] database cleanups. If follow-up actions are

required, refer the identified applications for additional review.

Agency Response: The Agency reported it identified the pending representative payee

applications before it completed scheduled database cleanups.

4. Determine whether there is a cost-effective method for identifying undocumented

representative payees and requiring such payees to account for the use of benefits they

receive on the behalf of child beneficiaries.

Agency Response: SSA published an Administrative Message to remind technicians how to

get proper documentation on accounting forms from undocumented representative payees.

5. Determine whether it is cost-effective to periodically review a list of children under age 18 in

direct pay status as a monitoring control. At a minimum, we believe all children under

age 15 without a representative payee should be identified on a periodic basis so that payees

can be appointed.

Agency Response: The Agency reported it reviewed its policies and procedures and, given

the budget climate and other pressing systems and operational activities in the representative

payee area, it did not believe it would be cost-effective to periodically review the cases of

children under age 15 without representative payees. However, SSA published an

administrative message

3

to remind employees about the need to select representative payees

as soon as possible for children under age 15.

3

SSA, AM-12084, Reminder-Issuing Direct Payments for Child Beneficiaries Under Age 18 and Reinstating

Benefits Timely (July 20, 2012).

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) B-1

– SCOPE AND METHODOLOGY

To accomplish our objective, we:

Obtained and reviewed applicable Federal laws and regulations and the Social Security

Administration’s (SSA) policies and procedures.

Reviewed a prior Office of the Inspector General report on minor children receiving benefits

without representative payees.

Met with personnel from SSA’s Office of the Deputy Commissioner for Operations.

Obtained and analyzed electronic data extracts from SSA’s Master Beneficiary and

Supplemental Security Records. See Appendix C for detailed information.

Performed data mining to identify two mutually exclusive sampling frames for review. See

Appendix C for detailed information.

One sample frame consisted of 709 minor children under age 15 who had no

representative payees as of April 2017.

Another sample frame consisted of 1,273 minor children between ages 15 and 17 and

5 months who had no representative payees as of April 2017.

Submitted information for 709 minor children under age 15 without representative payees to

the Agency for review.

Reviewed information for 118 of the 709 minor children under age 15 and determined

whether individuals other than the child were receiving payments. For these items, we

examined information from the Treasury Check Information System to determine who

received the benefits. Additionally, we reviewed SSA’s Electronic Representative Payee

System (eRPS) to determine whether SSA appointed representative payees for children

before our submitting information for the 709 minor children under age 15.

Determined whether we identified items in this sampling frame in the prior audit.

1

Selected a random sample of 50 minor children between ages 15 and 17 and 5 months and

50 minor children under age 15 without representative payees and determined compliance

with SSA’s policies.

For sample items, we examined information from eRPS, the Claims File User Interface,

and the Modernized Supplemental Security Income Claims System. Additionally, we

reviewed queries from SSA’s Master Beneficiary and Supplemental Security Records.

We reviewed this information to determine whether SSA complied with policies and

procedures and appointed representative payees for minor children when required.

Determined whether we identified items in this sampling frame in the prior audit.

2

1

SSA, OIG, Minor Children Receiving Benefits Without a Representative Payee, A-13-10-10104 (May 2011).

2

See Footnote 1.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) B-2

Calculated payments for minor children who received benefits without representative payees

when SSA policy required the children have representative payees.

We conducted our review from June 2017 through September 2018 at SSA Headquarters in

Baltimore, Maryland. The principal entity audited was the Office of the Deputy Commissioner

for Operations.

We determined the computer-processed data used for this audit were sufficiently reliable to meet

our audit objectives. Further, any data limitations were minor in the context of this assignment,

and the use of the data should not lead to an incorrect or unintentional conclusion.

We conducted this performance audit in accordance with generally accepted government

auditing standards. Those standards require that we plan and perform the audit to obtain

sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions

based on our audit objectives. We believe that the evidence obtained provides a reasonable basis

for our findings and conclusions based on our audit objectives.

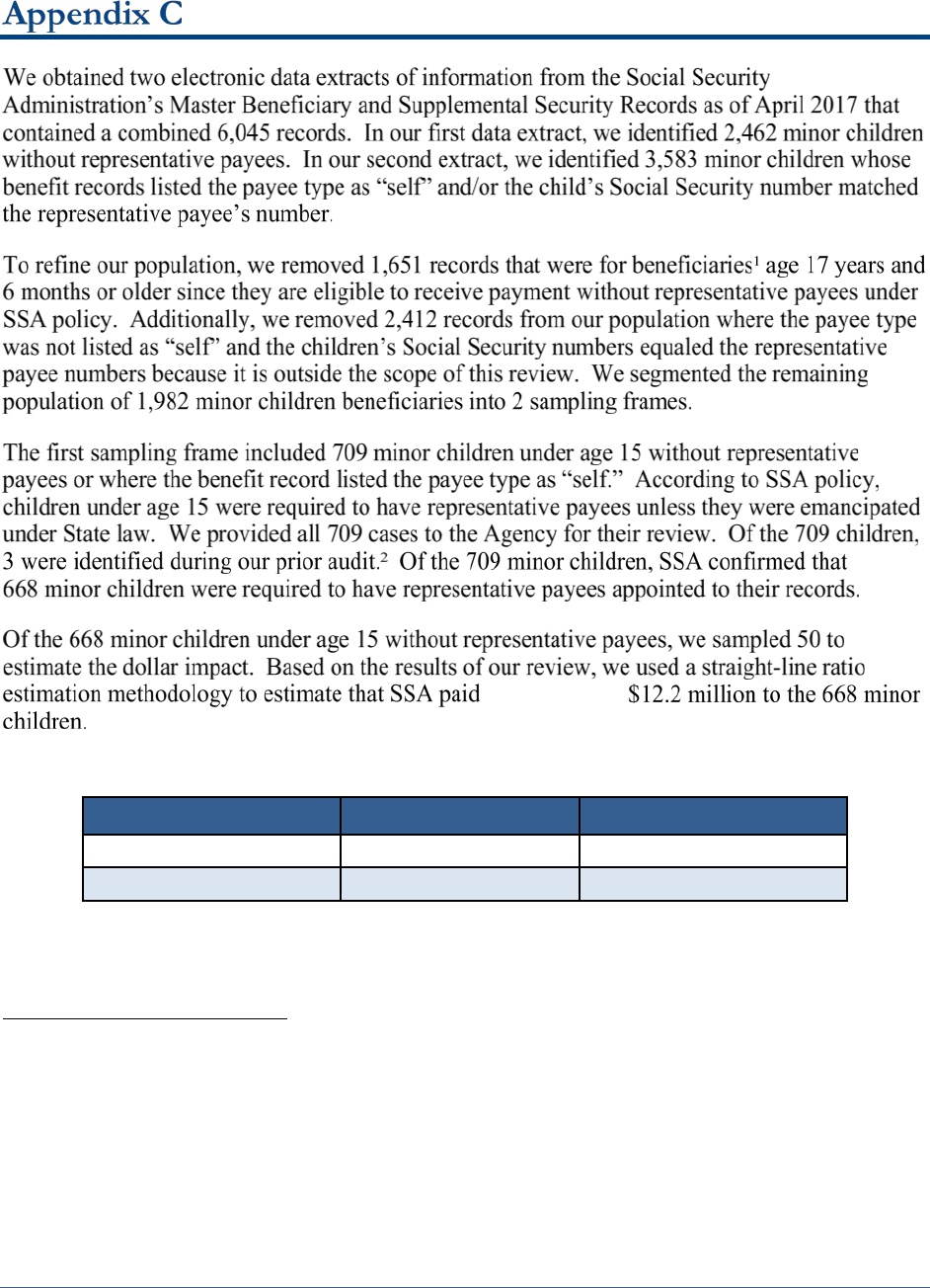

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) C-1

– SAMPLING METHODOLOGY AND RESULTS

approximately

Table C–1: Straight-line Estimation for Sample Frame 1

Description Sample Cases 668 Beneficiaries

Sample Size

50

668

Payments

$914,291

$12,214,921

3

1

We use the term “beneficiary” generically in this report to refer to both Old-Age, Survivors and Disability

Insurance beneficiaries and Supplemental Security Income recipients.

2

SSA, OIG, Minor Children Receiving Benefits Without a Representative Payee, A-13-10-10104, (May 2011).

3

To calculate the estimated amount of benefits, we determined the average payment per beneficiary for the

50 sample cases of minor children under age 15 ($914,290.50 / 50 = $18,285.81). We then multiplied the average

payment per beneficiary by the number of minor children under age 15 who are required to have representative

payees ($18,285.81 x 668 = $12,214,921.08).

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) C-2

approximately

Table C–2: Projections for Sample Frame 2

Description

Number of

Children

Amount of Payments

Sample Results

32

$883,707

Point Estimate

815

$22,499,184

Projection Lower Limit

658

$15,292,465

Projection Upper Limit

955

$29,705,903

Note: All statistical projections were calculated at the 90-percent confidence level.

Additionally, we used a straight-line ratio estimation methodology to estimate that SSA did not

properly document capability determinations for 356 children.

Table C–3: Straight-line Estimation for Sample Frame 2

Description

Sample Cases

Beneficiaries

Sample Size

50

1,273

Results

14

356

5

4

We identified six children from the prior audit in this group of beneficiaries.

5

To calculate the estimated amount of beneficiaries whose capability determinations SSA did not properly

document, we first calculated 1,273 x 14 = 17,822. We then divided the 17,822 by the number in our sample size

(17,822 / 50 = 356.44). We rounded the 356.44 down to 356.

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) D-1

– AGENCY COMMENTS

SOCIAL SECURITY

MEMORANDUM

Date:

May 6, 2019 Refer To: S1J-3

To:

Gail S. Ennis

Inspector General

From:

Stephanie Hall

Acting Deputy Chief of Staff

Subject:

Office of the Inspector General Draft Report “Follow-up: Minor Children Receiving Social

Security Payments Without a Representative Payee” (A-13-17-50169) -- INFORMATION

Thank you for the opportunity to review the draft report. Please see our attached comments. We

also provided technical comments at the staff level.

Please let me know if we can be of further assistance. You may direct staff inquiries to Trae

Sommer at (410) 965-9102.

Attachment

Minor Children Receiving Social Security Benefits Without a Representative Payee (A-13-17-50169) D-2

SSA COMMENTS ON THE OFFICE OF THE INSPECTOR GENERAL DRAFT

REPORT, “MINOR CHILDREN RECEIVING SOCIAL SECURITY PAYMENTS

WITHOUT A REPRESENTATIVE PAYEE” (A-13-17-50169)

GENERAL COMMENTS

We are continuing our efforts to implement the changes required by the Strengthening

Protections for Social Security Beneficiaries Act of 2018. With the enactment of the new law,

two Sections (Section 201: Advance Designation of Representative Payee and Section 204:

Reassessment of Payee Selection and Replacement Policies) of the law affect our current policies

on capability determination for minor children, as well as determining or adjudicating the proper

selection of a representative payee. Emancipated minors (below age 18) will have the ability to

make an advance representative payee designation that will take precedence over the current

order of preference. We expect to publish updated instructions and provide training to field

office staff on the changes by the end of fiscal year 2019.

Our responses to the recommendations are below.

Recommendation 1

Direct employees to (1) comply with policies for appointing representative payees for minor

children, (2) document capability determinations, and (3) adjudicate representative payee

applications properly.

Response

We agree.

Recommendation 2

Implement a process to periodically identify all children under age 17 and 5 months being paid

directly; and determine and document whether the Agency needs to appoint representative

payees.

Response

We agree.

MISSION

By conducting independent and objective audits, evaluations, and investigations, the Office of

the Inspector General (OIG) inspires public confidence in the integrity and security of the Social

Security Administration’s (SSA) programs and operations and protects them against fraud,

waste, and abuse. We provide timely, useful, and reliable information and advice to

Administration officials, Congress, and the public.

CONNECT WITH US

The OIG Website (https://oig.ssa.gov/) gives you access to a wealth of information about OIG.

On our Website, you can report fraud as well as find the following.

• OIG news

• audit reports

• investigative summaries

• Semiannual Reports to Congress

• fraud advisories

• press releases

• congressional testimony

• an interactive blog, “

Beyond The

Numbers” where we welcome your

comments

In addition, we provide these avenues of

communication through our social media

channels.

Watch us on YouTube

Like us on Facebook

Follow us on Twitter

Subscribe to our RSS feeds or email updates

OBTAIN COPIES OF AUDIT REPORTS

To obtain copies of our reports, visit our Website at https://oig.ssa.gov/audits-and-

investigations/audit-reports/all. For notification of newly released reports, sign up for e-updates

at https://oig.ssa.gov/e-updates.

REPORT FRAUD, WASTE, AND ABUSE

To report fraud, waste, and abuse, contact the Office of the Inspector General via

Website: https://oig.ssa.gov/report-fraud-waste-or-abuse

Mail: Social Security Fraud Hotline

P.O. Box 17785

Baltimore, Maryland 21235

FAX: 410-597-0118

Telephone: 1-800-269-0271 from 10:00 a.m. to 4:00 p.m. Eastern Standard Time

TTY: 1-866-501-2101 for the deaf or hard of hearing